If only every quarter was like the previous one! My net worth plunged by $130k this quarter, largely due to crypto lol. Now that I’m paying rent, I don’t have a lot of spare cash to invest so net worth has stagnated.

| Asset Class | April 3rd 2021 | July 17 2021 | Change | Notes |

| Business cash | $22.8k | $10k | -$13k | Business has been unprofitable recently (more below) |

| Business investments | $20.6k | $0 | -$20.6k | Sold all investments in business |

| Personal cash reserve | $17k | $6k | -$11k | Bought some shares in the startup I work for |

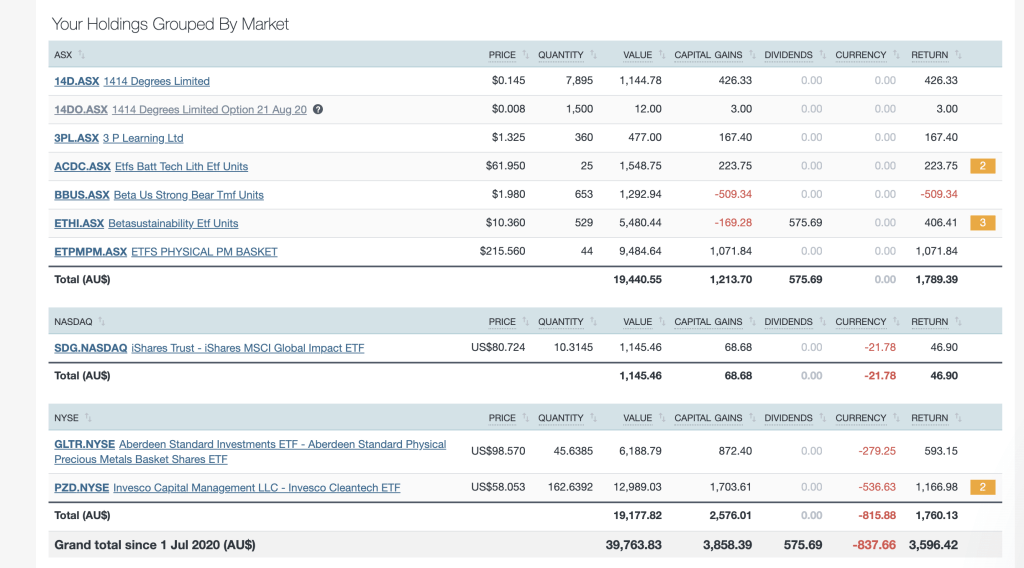

| Cryptoassets | $150k | $60k | -$90k | Fun volatility here! |

| Property (brickX) | $10.2k | $10.9k | +$0.7k | Minimal growth |

| Precious metals | $18.5k | $19.9k | +$1.4k | Steadily buying more |

| Shares | $75.7k | $68.35k | -$7k | Sold some shares to prop up business |

| Green bonds | $12k | 0 | No change | |

| Super | $125k | $137k | +$12k | Investment growth – only compulsory contributions now |

| HELP debt | -$11k | -$8k? | +$3k | Paying it down gradually |

| Net worth | $444k | $315k | -$330k |

Expenses

Personal

Joint

Life update

We’ve settled down in Melbourne. Pretty happy here. Nice to be close to family. My expenses are up quite a lot as we’re paying rent now but it was a bit of an unrealistic arrangement before when we were living in my wife’s apartment in Sydney and I wasn’t contributing at all for various reasons. She’s renting the Sydney apartment out now which is a net positive for our cashflow as a couple.

I’m restarting my TAFE course (Cert III in Carpentry) this week which I’m looking forward to.

Career update

Still in the same situation as in my last update: working 3 days per week in my solar job (which I’m enjoying) and 1 day per week for my old job. Balancing it all remains tricky particularly now that I’m starting the TAFE course again.

Business update

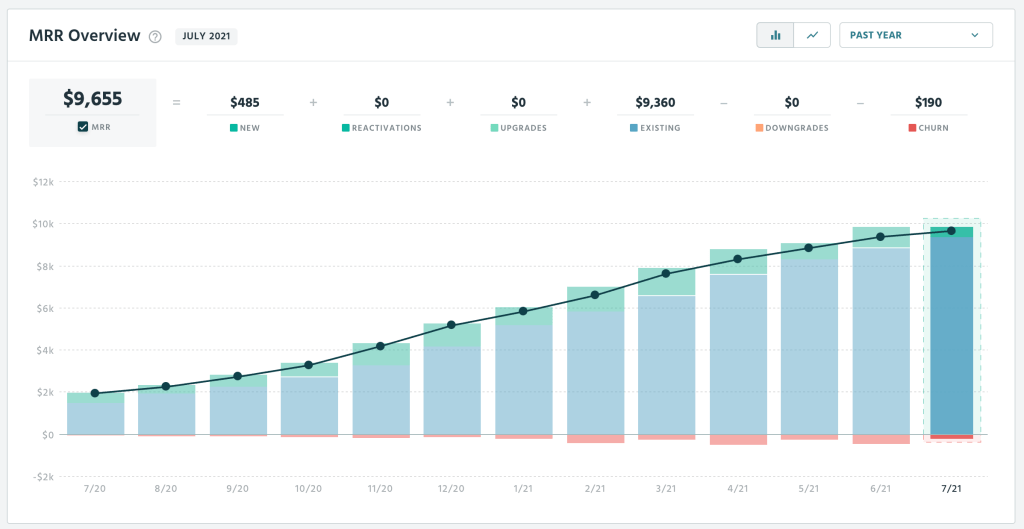

Revenue has been increasing but I’m still running at a loss. I’ve burnt down all the cash reserves in my business and have had to put $8k of my personal cash in. I’m anticipating having to put another $15k in before the end of the year at which point it should reach break even.

Revenue in USD

Overall, I made a $6k loss in the business last year.

Revenue: $172k

Expenses: $191k (mostly subcontractors)

Non operating revenue: $12k (investment gains)

House update

We’re looking at buying a place to live in Melbourne. Quite captivated by the idea of getting a townhouse in Port Melbourne but I suspect that’s outside our budget (~$800k). Another option is to find a place by the beach quite far away from the city. Budget wise that would be great: we’d be able to get a place with a large block for $800k. I think I’d be very happy living in a small town and my wife is open to it but there is some difficulty about where her parents would live as they’re going to be moving to Australia soon (from China) and want to live close to us. I think they’d prefer to live somewhere like Springvale where there is a large Chinese speaking community. Many discussions to be had.

I’m pretty clueless when it comes to property so am listening to some podcasts and will probably do a course + engage a buyer’s advocate to help. Our timeframe is to make a purchase early next year.

Europe trip

Still keen to do a 12 month stint in Europe. Might do it at the start of 2023.

FI Goals

My (fat) FI number is $1.625M. 20% of the way there.

My coasting calculations indicate I’ll get there in 2042 assuming that I can get my business profit to $50k next year and keep it at that level until 2042 (I’d be 54). My wife will probably get there well before I do (2035).